AI Is Compressing Every Layer of Biotech Simultaneously. Here Is What That Means for Executives.

The conversation about AI in biotech has been about individual breakthroughs for years. A drug designed faster here. A clinical trial enrolled quicker there. A supply chain optimised at the margins. What is different now is not a single breakthrough. It is that every layer of the biotech value chain is being compressed by AI at the same time, and the business implications are starting to compound.

In the week of March 29 to April 5, 2026, four separate signals landed that, taken together, describe a structural shift. Insilico Medicine published its 2025 annual results. NVIDIA expanded BioNeMo with new life sciences partnerships. Tempus AI reported 27.31% improvement in clinical trial patient identification. EvolutionaryScale released ESM Cambrian, a new frontier in protein sequence modeling. These are not isolated news items. They are data points in the same pattern.

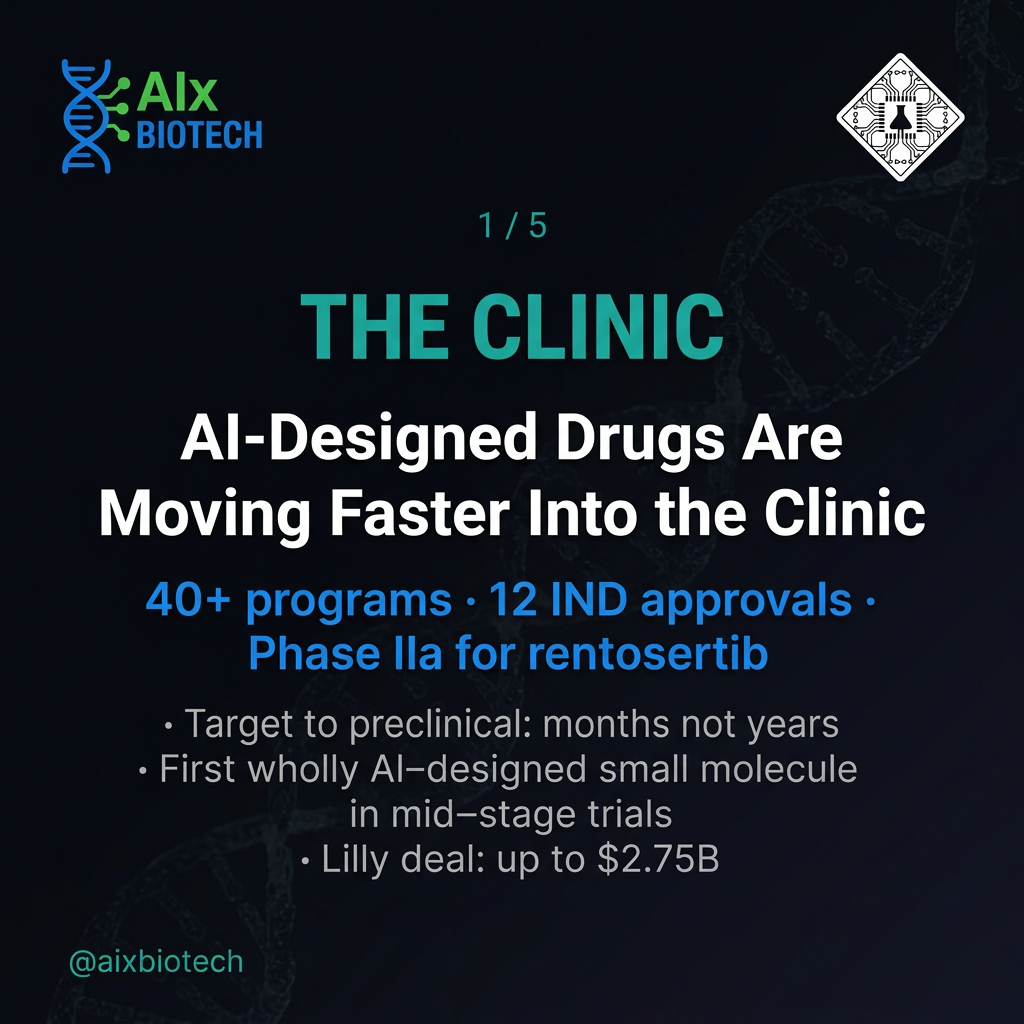

Signal 1: AI-Designed Drugs Are Moving Through the Clinic, Not Just the Lab

Insilico Medicine’s 2025 annual results, published March 29, 2026, are the clearest public benchmark for what AI-native drug discovery looks like at scale. The company now has over 40 total programs in its pipeline, with 12 IND approvals and 28 preclinical candidates nominated since 2021. In 2025 alone, they announced over 10 new collaborations totalling $1.3 billion in potential value. The Eli Lilly partnership, disclosed earlier this year, carries a value of up to $2.75 billion (Genetic Engineering and Biotechnology News, 2026).

The most significant data point is not the deal value. It is the Phase IIa results for rentosertib, which Insilico describes as the first wholly AI-discovered and AI-designed small-molecule drug to reach mid-stage clinical trials. That is not a claim about speed. It is a claim about the entire origin of the molecule. From target identification to chemical design to clinical candidate, the process was AI-driven.

For biotech executives watching pipeline economics, this matters because the cost structure of early-stage drug discovery is changing. If AI-native platforms can nominate preclinical candidates at higher velocity and lower cost per program, the portfolio logic of drug development changes with it. More shots on goal, distributed across more targets, at a fraction of the traditional per-program cost.

Signal 2: Big Pharma Is Embedding AI Into Core Pipelines, Not Pilots

Sanofi’s collaboration with BioMap is now publicly described as co-developing AI modules for biotherapeutic drug discovery, with potential value exceeding $1 billion (Klover AI, 2025). BioMap’s platform integrates large language models trained on biological data to accelerate target identification and molecule design across multiple therapeutic areas.

The framing matters. This is not a Sanofi pilot program or an innovation unit experiment. This is a core pipeline investment at the billion-dollar level. The same pattern is visible across AstraZeneca, Pfizer, and Novartis, all of which have disclosed material AI infrastructure commitments in the last 18 months.

The strategic implication for smaller biotech and mid-size pharma is a capability gap that is widening. Large pharma is building proprietary AI infrastructure at scale. The companies that do not have internal AI capabilities will either partner with platforms like BioMap, Insilico, or EvolutionaryScale, or they will compete with a slower, more expensive discovery process against organisations that have already compressed theirs.

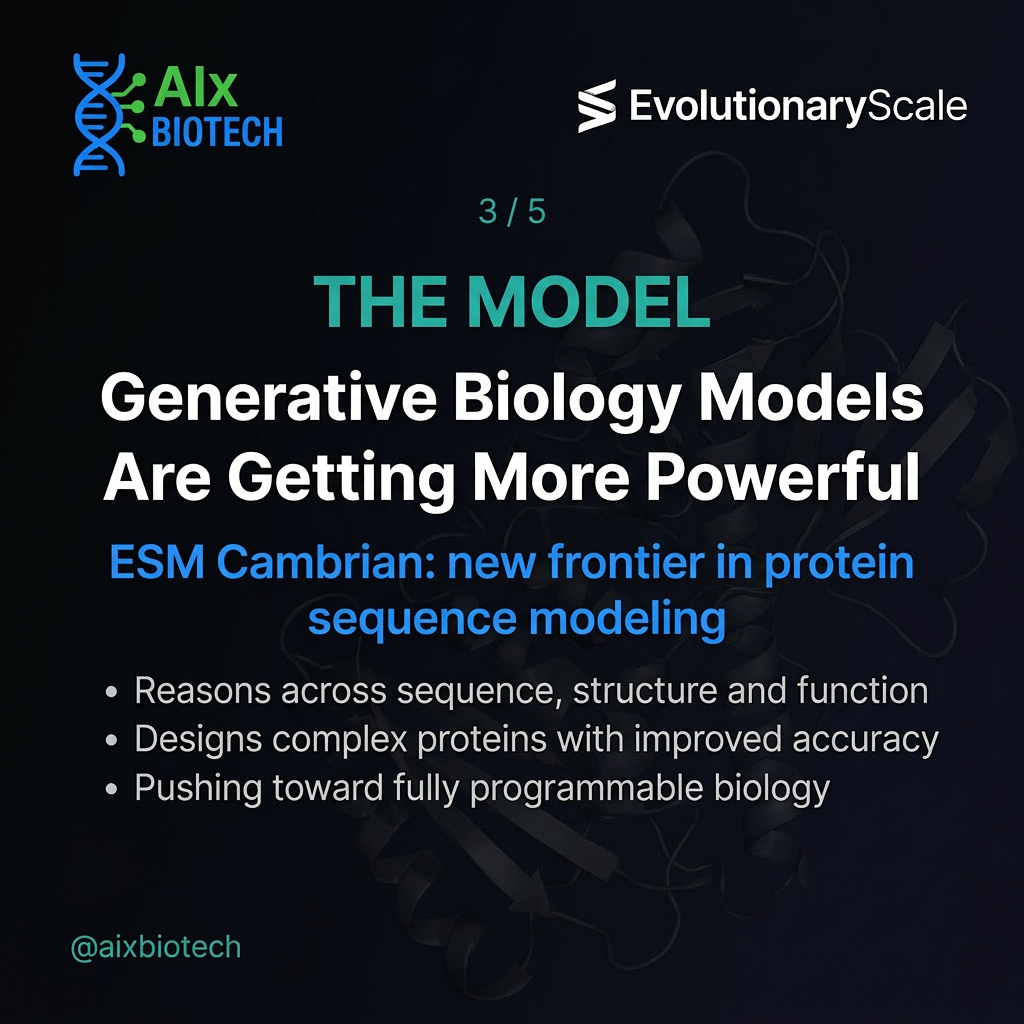

Signal 3: The Biology Modeling Layer Is Getting Significantly More Powerful

EvolutionaryScale released ESM Cambrian in early 2026, described as defining a new frontier in protein sequence modeling with breakthrough performance and efficiency. This follows ESM3, published in Science, which demonstrated the ability to reason simultaneously across protein sequence, structure, and function using a single generative model (Science, 2024).

The practical implication for drug discovery teams is that the design space for protein-based therapeutics is expanding. ESM3 and its successors can generate novel protein sequences with desired functional properties, predict structure from sequence with high accuracy, and do both in a fraction of the time and compute required by previous methods. For biologics programs, which represent a growing share of biotech pipelines, this is a direct capability upgrade.

NVIDIA’s January 12, 2026 announcement that BioNeMo is expanding to include RNA structure models, alongside the co-innovation AI lab launched with Eli Lilly, positions the compute and modeling infrastructure for biology as a genuine competitive asset. Jensen Huang publicly described 2026 as biology’s “transformer moment,” referencing the analogy to what large language models did for natural language processing. The BioNeMo platform is now adopted by multiple life sciences leaders for AI-driven drug discovery workflows (NVIDIA investor relations, January 2026).

Signal 4: Clinical Trial Bottlenecks Are Being Compressed Too

Tempus AI’s Tempus Link platform reported a 27.31% increase in patients identified as potential trial matches when AI-assisted matching was combined with registered nurse review, compared to standard identification processes (Tempus, 2025 clinical matching study). The company’s full year 2025 revenues reached $1.27 billion, with genomics testing revenue up 31.7% year-over-year in Q3 2025 alone.

Patient recruitment is where clinical timelines actually fail. As covered in this publication’s analysis of AI forecasting for specialty drug demand, the downstream commercial impact of a delayed trial is measured in months of lost exclusivity and hundreds of millions in NPV. A 27% improvement in patient identification at the front end of trial enrollment is not a marginal efficiency gain. It is a structural improvement in the probability that a trial completes on schedule.

The Tempus model is also instructive for how AI clinical tools get deployed in a regulated environment. The platform works within existing EHR workflows, routes identified patients to clinical nurse review before any contact is made, and operates on real-world data that has been collected and consented for research use. This is what compliant AI deployment in a clinical setting looks like. It is not an AI making clinical decisions. It is an AI doing the data pattern-matching work that was previously done manually and less accurately. For a practical framework on how biotech professionals can use AI tools within compliance boundaries, see the compliant path forward for pharma office workers.

Why This Is a Strategy Question, Not Just a Technology Question

Taken together, these four signals describe a biotech industry where AI is compressing timelines and costs at every stage simultaneously. Discovery. Protein design. Trial enrollment. Commercial forecasting. Infrastructure. When compression happens at multiple stages at once, the cumulative effect on development timelines and capital efficiency is not additive. It is multiplicative.

- The discovery-to-IND timeline is shortening: Insilico’s pipeline data suggests AI-native platforms can move from target identification to preclinical nomination in months rather than years. If IND applications are being submitted faster, trials start faster, and peak revenue is reached earlier. For a $1 billion peak revenue asset, pulling forward the launch date by 12 months is worth approximately $80 to $100 million in NPV terms.

- The compute infrastructure gap is becoming a competitive moat: NVIDIA’s positioning in life sciences is not a coincidence. The companies with the best AI infrastructure, proprietary biological training data, and GPU capacity are building capabilities that cannot be quickly replicated by organisations starting from zero. This is relevant for BD teams evaluating partnership targets and for investors assessing competitive durability.

- Trial enrollment is no longer the unmovable bottleneck it was: A 27% improvement in patient identification at Tempus scale, across a network of hundreds of oncology sites and millions of patient records, moves enrollment curves in ways that affect trial completion probability, not just speed. For biotech companies designing Phase II and Phase III protocols, AI-assisted site selection and patient identification should now be a standard component of the operational plan, not an optional upgrade.

- The capability gap between AI-native and legacy pharma is widening: The Sanofi-BioMap deal is not an outlier. It is one of dozens of large pharma AI infrastructure investments at the billion-dollar level that have been disclosed in the last 18 months. Smaller biotech and mid-size pharma that have not yet built or accessed comparable AI capabilities are competing on slower timelines, at higher per-program costs, against organisations that have already compressed theirs.

The Question Allard de Jong Posed This Week

The signal that generated the most engagement this week came with a question attached: if AI removes the biggest bottlenecks in biotech, what becomes the new limiting factor?

The honest answer is that it is not yet clear, and that ambiguity is itself strategically important. When the binding constraint shifts, organisations that identified the new constraint first and built capability around it early extract disproportionate value. The candidates for the new limiting factor include access to proprietary biological data of sufficient quality and scale to train meaningful models, regulatory infrastructure that can keep pace with AI-accelerated development timelines, and manufacturing capacity for the biologics and cell and gene therapies that AI-designed pipelines are increasingly producing.

None of these is a technology problem. They are operational, regulatory, and capital allocation problems. Which means the competitive advantage in the next phase of AI in biotech may accrue not to the best model builders, but to the organisations that solve the non-technological constraints first.

Key Takeaway

The lab is no longer the bottleneck. The compression is real, it is simultaneous across multiple stages, and the business implications are compounding. Biotech executives who are still treating AI as a discovery-stage tool are looking at only one layer of a stack that is being rebuilt end to end. The organisations that are building AI capability across discovery, clinical operations, and commercial planning at the same time are not just moving faster. They are changing the economics of the entire business.

Frequently Asked Questions

What does Insilico Medicine’s 2025 annual results tell us about AI drug discovery timelines?

Insilico’s results show 40+ total programs, 12 IND approvals, and 28 preclinical candidates nominated since 2021, with over $1.3 billion in new collaborations signed in 2025. Phase IIa results for rentosertib, the first wholly AI-discovered small molecule to reach mid-stage trials, provide the most concrete public data point on what AI-native discovery timelines look like at scale. The trajectory from target to IND is compressing from years to months for AI-native platforms.

How does Tempus AI’s 27% patient identification improvement affect trial timelines?

A 27.31% increase in patient identification means more eligible patients are found earlier in the enrollment process. For trials where recruitment failure is the primary cause of delay, this directly improves the probability that enrollment completes on schedule. The downstream effect on development timelines and commercial NPV is material, particularly for biomarker-selected oncology and rare disease programmes where the eligible population is small and dispersed.

What is NVIDIA BioNeMo and why does it matter for biotech?

BioNeMo is NVIDIA’s open development platform for AI-driven biology and drug discovery. As of January 2026, it is being adopted by multiple life sciences leaders and is expanding to include RNA structure models. The platform provides the compute infrastructure and pretrained biological models that drug discovery teams need to run AI workflows at scale. The co-innovation lab with Eli Lilly, announced January 12, 2026, signals that the largest pharma companies are building proprietary AI infrastructure on top of NVIDIA’s platform rather than building from scratch.

Based on publicly available information. This analysis covers non-proprietary, publicly disclosed data only. References: Insilico Medicine Annual Results (March 2026), Genetic Engineering and Biotechnology News (2026), NVIDIA Investor Relations (January 2026), Tempus AI clinical matching study (2025), Tempus AI FY2025 Results, Klover AI Sanofi analysis (2025), EvolutionaryScale ESM Cambrian release (2026), Science journal ESM3 (2024).