The 2025 Drug Sales Ranking Is a Commercial Disruption Map

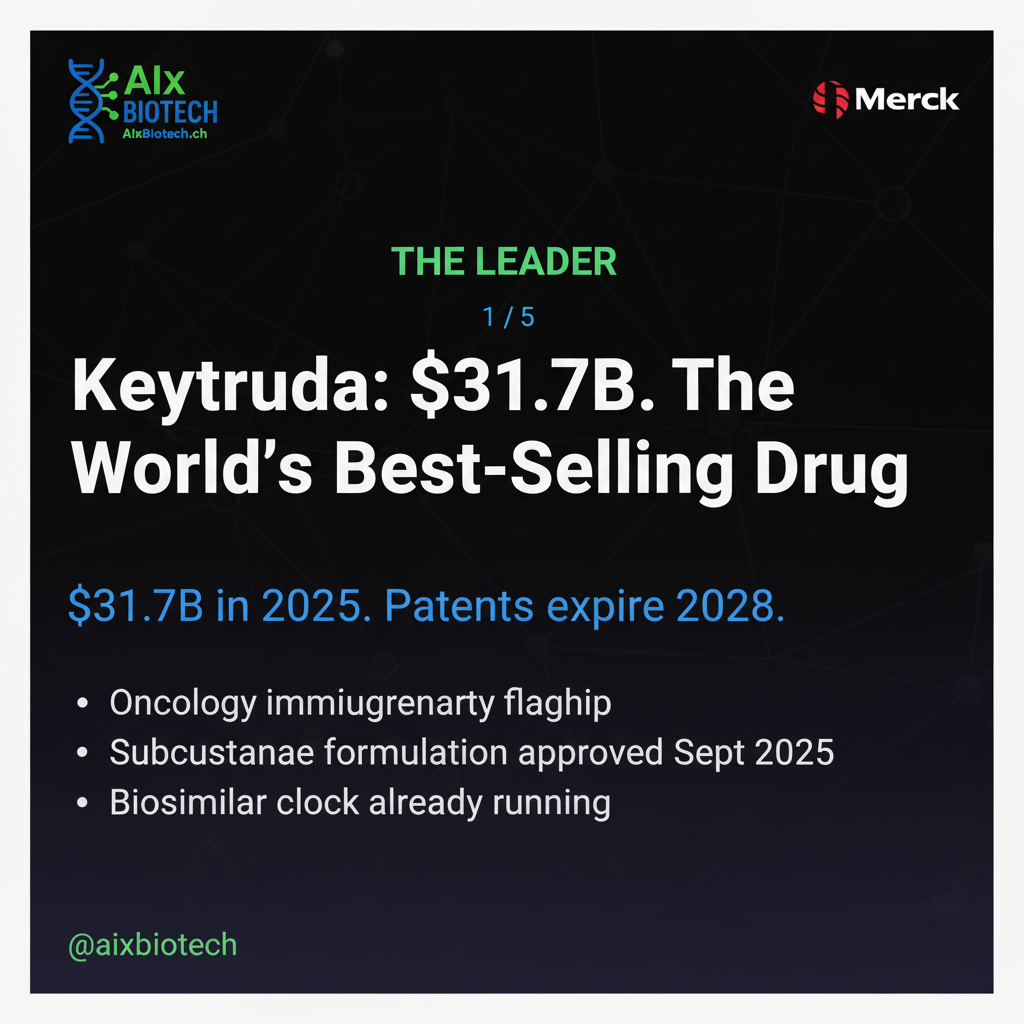

Keytruda held the top spot at $31.7 billion. Mounjaro came in second at $23 billion. Humira, once the world’s best-selling drug at $21 billion, closed 2025 at $4.5 billion.

Most people read this ranking as a sales leaderboard. Our team at AIxBiotech reads it as a commercial disruption map. Three structural shifts are visible in this data that will reshape biotech commercial strategy over the next three years.

Shift One: GLP-1s Are Becoming the Largest Commercial Infrastructure in Pharma

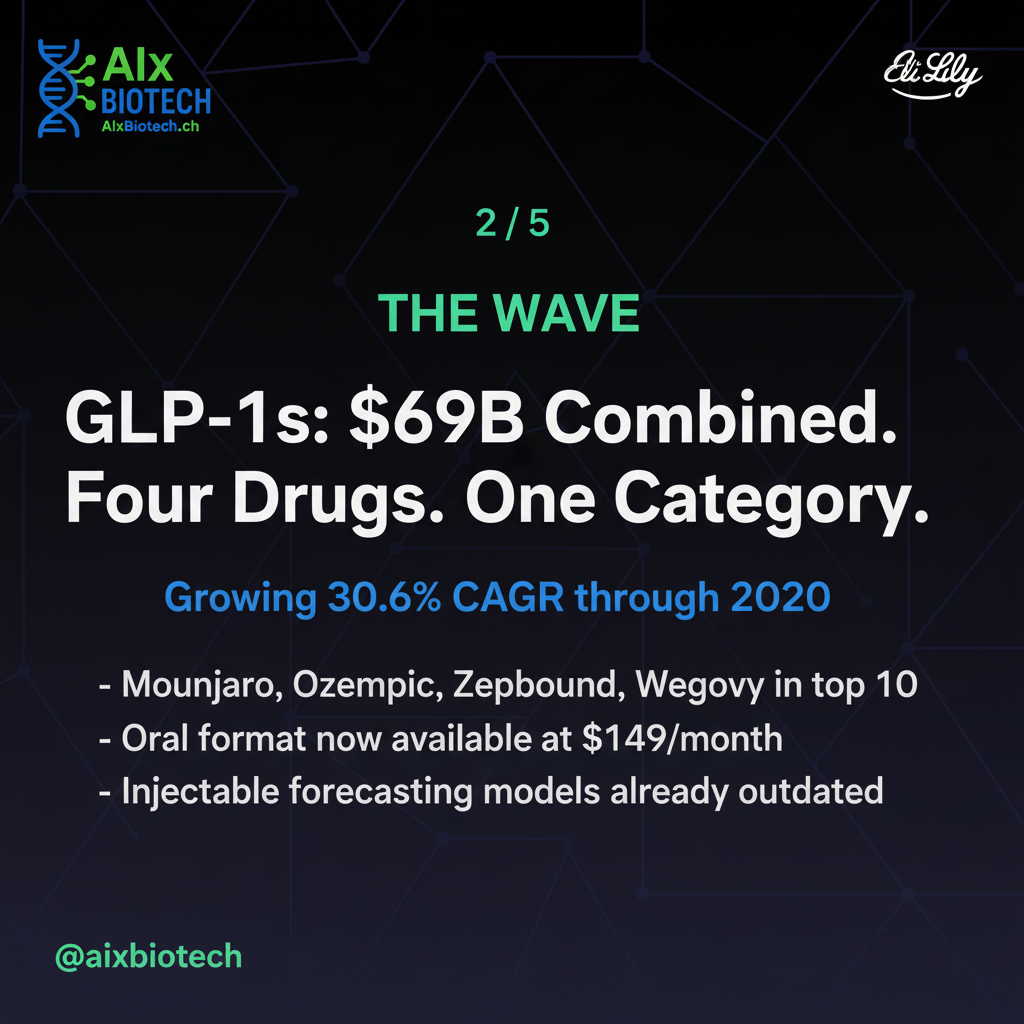

Four drugs in the top 10 are GLP-1 receptor agonists. Mounjaro at $23 billion, Ozempic at $20.1 billion, Zepbound at $13.5 billion, and Wegovy at $12.5 billion. Combined 2025 sales: approximately $69 billion. Growing at a 30.6% CAGR through 2030 according to BCC Research.

This is no longer a therapeutic category. It is a commercial infrastructure problem. Cold chain logistics, specialty pharmacy distribution, patient adherence programmes, and direct-to-consumer channels are all being rebuilt at a scale pharma has not seen since statins.

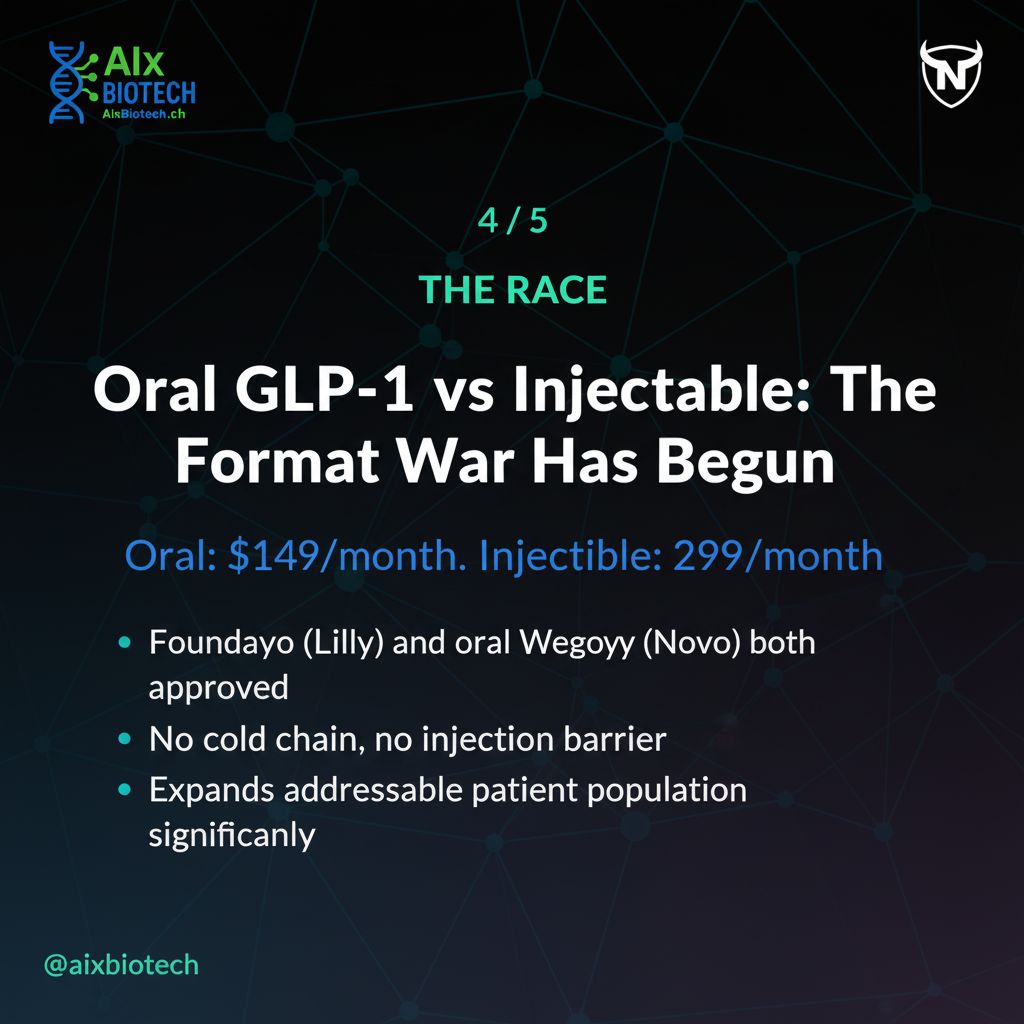

The oral format accelerates this further. Lilly’s Foundayo (orforglipron) received FDA approval on April 1, 2026. Novo Nordisk’s oral Wegovy was approved in December 2025. As detailed in our analysis of Lilly’s Foundayo approval and what it means for the GLP-1 commercial playbook, self-pay pricing for oral formulations starts at $149 per month versus $299 for injectable Zepbound. Oral delivery removes cold chain dependency, simplifies pharmacy distribution, and expands the addressable patient population to people who will not self-inject.

Snapshot: GLP-1 combined 2025 sales exceed $69 billion across four products. Oral formulations now available at $149 per month self-pay.

For commercial teams building GLP-1 infrastructure: AI demand forecasting models calibrated on injectable volume will need recalibration as oral market share grows. The transition is not a future event. It is already underway.

Shift Two: Keytruda Is at Its Commercial Peak

At $31.7 billion, Keytruda is the single best-selling drug in the world. It is also approaching a cliff. US primary patents expire in late 2028. Biosimilar manufacturers are already filing. Merck’s response, a subcutaneous formulation approved by the FDA in September 2025 using Halozyme’s ENHANZE technology, buys time through extended patent protection but does not eliminate the structural risk.

The commercial implication for biotech teams is less about Merck specifically and more about what replaces Keytruda-level oncology revenue in portfolios that depend on it. AI-assisted BD tools are already scanning competitive pipeline data, patent filings, and regulatory signals to identify next-generation I/O assets before they reach Phase III pricing. As explored in our piece on why the rNPV spreadsheet is no longer enough for biotech valuation, the window between mid-stage validation and contested acquisition target is closing fast in the post-Keytruda oncology landscape.

Key signal: Keytruda US patents expire late 2028. Merck SC formulation approved September 2025 extends protection. Biosimilar filings already in progress.

Shift Three: Humira Is the Biosimilar Playbook

Humira peaked at $21 billion in 2022. By 2025 it had fallen to $4.5 billion. That is a 78% revenue erosion in three years following US exclusivity loss in early 2023. According to AbbVie guidance, Humira usage is expected to drop to 12% of its addressable market by mid-2025.

AbbVie survived the erosion because Skyrizi reached $17.5 billion and Rinvoq reached $8.3 billion in 2025, both appearing in the top selling drugs ranking in their own right. Most companies that face biosimilar competition at scale will not have that cushion already generating revenue.

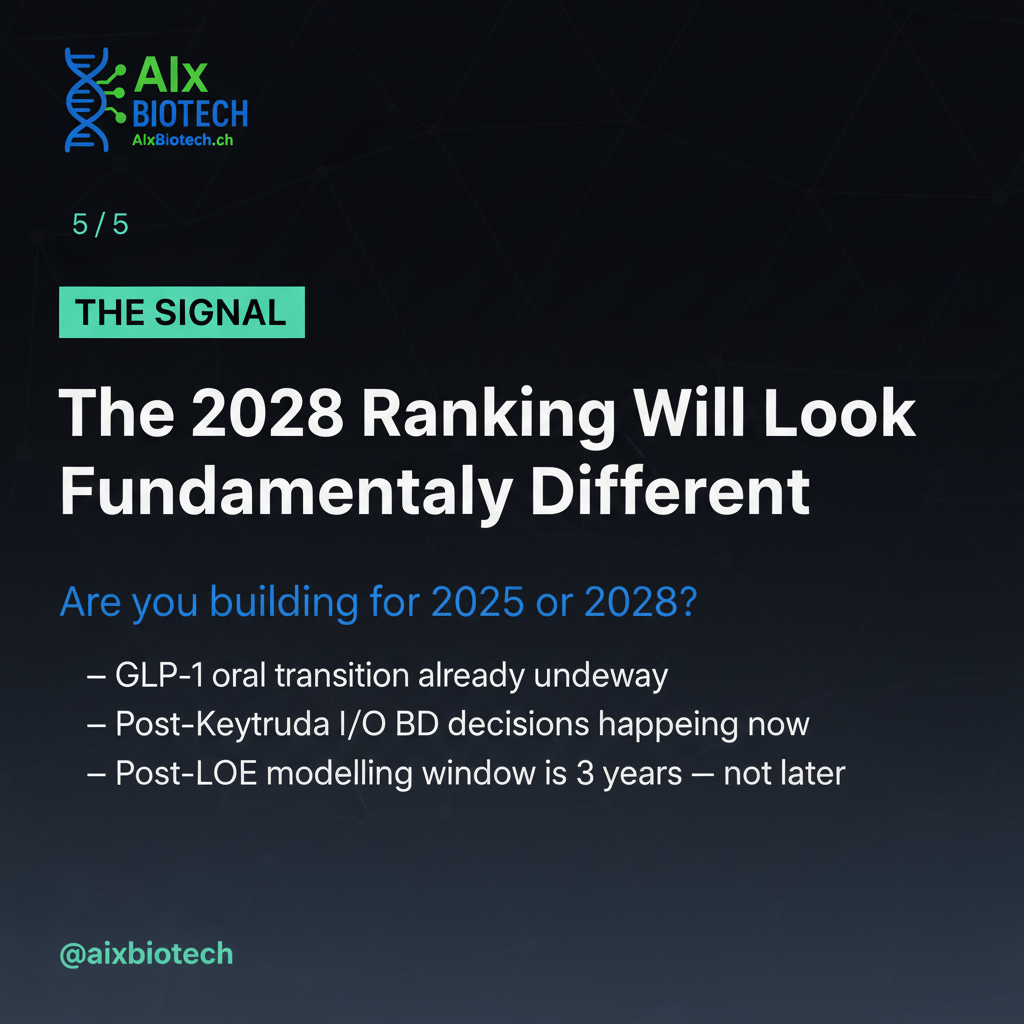

The operational lesson is clear. The three years before exclusivity loss are not a wind-down period. They are a commercial rebuild window. AI scenario modelling tools that simulate post-LOE revenue trajectories are now standard practice at large pharma. They should be standard practice for any biotech with a biologic approaching patent expiry in the 2027 to 2030 window.

What Commercial Teams Should Do Right Now

- GLP-1 commercial teams: Audit your demand forecasting models for oral market entry assumptions. Injectable volume projections from 2024 are already outdated.

- Oncology commercial and BD teams: The post-Keytruda I/O landscape is being shaped by decisions made today. AI pipeline intelligence tools are no longer optional.

- Any team with a biologic in the 2027 to 2030 expiry window: Start post-LOE commercial scenario modelling now. Three years moves faster than it looks from today.

FAQ

Why did GLP-1 drugs dominate the 2025 ranking so quickly?

GLP-1 drugs address obesity and metabolic disease at a scale no prior therapy has matched. The combination of strong clinical outcomes, broad patient eligibility, and direct-to-consumer channels drove unprecedented commercial velocity. The oral transition is now accelerating adoption further by removing the injection barrier.

How serious is the Keytruda patent cliff for oncology commercial teams?

Serious but not immediate. US primary patents expire in late 2028. Merck has taken steps to extend protection through new formulations. However, biosimilar filings are already in motion and commercial teams planning 2028 to 2030 oncology portfolios need to model post-Keytruda scenarios now rather than closer to expiry.

What is the core lesson from Humira’s biosimilar erosion?

The core lesson is that biosimilar erosion is fast and structural once it starts. AbbVie’s survival depended on next-generation assets that were already generating significant revenue before Humira’s exclusivity loss. Biotech companies approaching patent expiry need replacement revenue generating, not just in pipeline, before the cliff arrives.

Should AI tools be used for post-LOE scenario modelling?

Yes. AI scenario modelling tools can simulate post-exclusivity revenue trajectories across multiple biosimilar entry assumptions, price erosion rates, and market segment dynamics. These tools do not touch regulated or patient-level data and can run on commercial and market intelligence data that is publicly available or internally generated in non-regulated systems.

The 2025 ranking is a snapshot. The 2028 ranking will look fundamentally different. The commercial teams building AI infrastructure today are positioning for that version of the market.

Based on publicly available information. Sales figures sourced from company earnings reports and IQVIA Institute data 2025. This analysis covers non-proprietary, publicly disclosed data only.