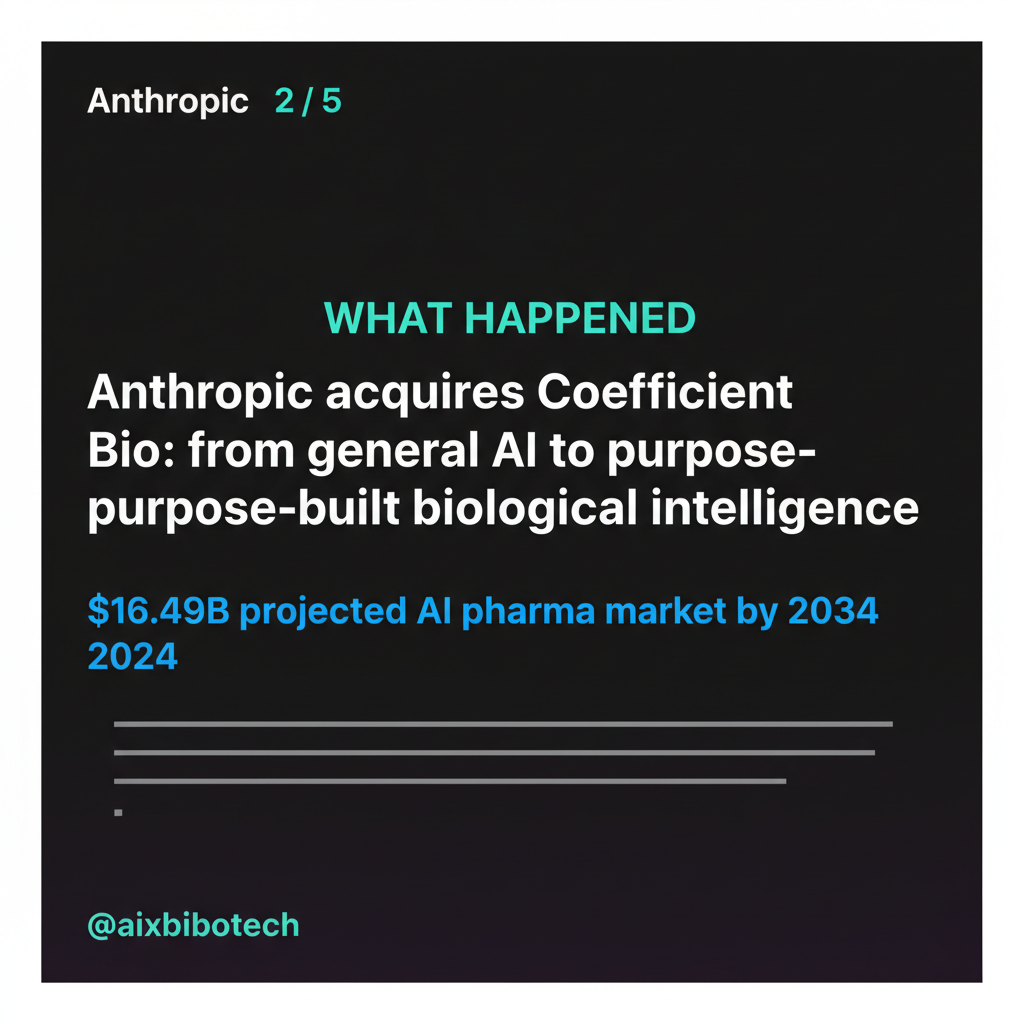

Anthropic acquires Coefficient Bio for $400M: what it means for AI drug discovery

Anthropic has acquired Coefficient Bio, an AI biotech startup with fewer than 10 employees, for over $400 million in stock. The company had been operating in stealth for just eight months. It had no publicly disclosed product and no commercial revenue.

The price is extraordinary. The implications are larger than the price.

What Anthropic actually bought

Coefficient Bio’s team consists almost entirely of former computational biology researchers from Genentech’s Prescient Design unit. These are specialists in biological foundation models and biomolecule design. Not general AI researchers. Not software engineers. Scientists who spent years building the specific type of AI models that predict protein structure, design novel molecules, and model biological systems at scale.

Anthropic’s stated goal for the acquisition is to build AI models and platforms from scratch specifically for biological research, rather than adapting its existing Claude models for science through third-party partnerships. The Coefficient Bio team will work directly within Anthropic’s life sciences division and contribute to its “Claude for Life Sciences” programme.

This is a fundamental shift in strategy. Adapting general models creates a dependency on external partners and limits how deeply the AI can be specialised for biological tasks. Building from the ground up means Anthropic controls the entire stack: the data, the architecture, the training process, and the outputs.

Key signal: The AI pharmaceuticals market is projected to reach $16.49 billion by 2034. Generative AI in drug discovery alone is projected at $2.85 billion. Anthropic’s $400 million investment is a claim on a structurally large and growing market. Source: publicly available market research, 2025.

The competitive landscape just shifted

Anthropic’s move completes what is now a clear pattern. Every major foundation model company is building a direct capability in biotech AI.

Google DeepMind created Isomorphic Labs as a standalone AI drug discovery company, building on the AlphaFold foundation. Nvidia committed over $1 billion to its partnership with Eli Lilly, embedding its computing infrastructure directly into Lilly’s drug discovery pipeline. OpenAI announced an embedded collaboration with Moderna for mRNA design and clinical development.

Now Anthropic has Coefficient Bio. The foundation model companies are no longer positioning themselves as infrastructure providers to biotech. They are positioning themselves as direct participants in drug discovery.

This has a specific implication for biotech commercial and BD teams. The partnership agreements that will define competitive advantage over the next decade are being signed now. Companies that access these platforms early, on favourable terms, are building capabilities that will compound. Companies that wait are entering a more competitive and expensive market.

What this means for biotech executives today

There are three practical considerations for biotech leaders watching this deal.

First, the acqui-hire valuation signals how scarce specialized biological AI expertise is. Venture firm Dimension reportedly saw a substantial return on its investment in a startup that was eight months old. That pricing reflects genuine scarcity, not speculative excess. If your commercial or R&D team is trying to build in-house AI capability, the talent market you are competing in is the same one where Anthropic just paid $40 million per person.

Second, the shift from adapting general AI to building purpose-built biological AI is the most important technical development of this year. General models can answer biotech questions. Purpose-built models can generate novel biology. The difference in commercial value is enormous. Watch which AI partnerships your competitors are signing. The ones with access to purpose-built biological AI will have a structurally different R&D productivity curve.

Third, the compliance and data governance question becomes more urgent. As AI companies move deeper into drug discovery, the boundary between public research AI and regulated proprietary data becomes harder to manage. Any engagement with foundation model companies for drug discovery purposes requires rigorous separation of public research data from IND-stage pipeline data, trade secrets, and proprietary compound libraries. GxP and 21 CFR Part 11 compliance requirements apply to any AI system used in regulated activities, regardless of who built it.

As our team covered in the analysis of AI vendor due diligence for biotech executives, the four questions that matter most when evaluating any AI partner include exactly this: where does your data go and who has access to it?

FAQ

Why did Anthropic pay $400M for a team of fewer than 10 people?

The valuation reflects the extreme scarcity of researchers who can build biological foundation models. Former Genentech Prescient Design researchers have a specific skill set that is not replicable by hiring general AI engineers. Anthropic paid for a capability that would take years to build from scratch internally.

How does this compare to Google DeepMind’s Isomorphic Labs?

Isomorphic Labs was spun out of DeepMind with AlphaFold as its foundation and has signed major licensing deals with Eli Lilly and Novartis. Coefficient Bio is earlier stage and will operate inside Anthropic rather than as a standalone company. The strategic intent is similar but the execution model differs.

Does this deal affect current Claude for Life Sciences users?

Anthropic has indicated the Coefficient Bio team will strengthen Claude for Life Sciences. Users should expect more biologically specialised capabilities over time, but existing partnerships and API access are not expected to change in the near term.

Should biotech companies start AI drug discovery partnerships now?

The window for early-mover partnerships on favourable terms is narrowing. Companies that establish these relationships now, when the platforms are still being defined, have more ability to shape the terms. This is a BD and licensing strategy question as much as a technology question.

The foundation model companies have decided that drug discovery is their next major market. That is a signal worth taking seriously.

Based on publicly available information. This analysis covers non-proprietary, publicly disclosed data only.